Government Debt Isn't the Problem—Private Debt Is

The Roaring Twenties, the Japanese boom of the '80s, and the U.S.'s in the early 2000s have one thing in common: They were debt-fueled binges that brought these economies to the brink of ruin.

Former Fed Chairman Alan Greenspan, discussing the financial crisis of 2008, wrote that “financial bubbles occur from time to time, and usually with little or no forewarning.”

That’s misleading at best. The 2008 collapse was predictable. And, more generally, major financial crises of this type can be seen well in advance—and prevented—if you know what to look for. In fact, there’s a fairly simple formula that predicts such crises with a high amount of confidence. And it suggests that the world economy remains in more peril than is generally appreciated.

This conclusion comes from an examination of financial crises around the world, dating back to the 19th century, that I conducted with my colleagues and summarize in my new book The Next Economic Disaster. The logic behind our conclusion can be seen in the diagrams below.

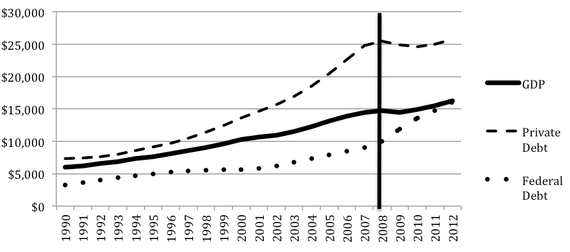

Take a look at this graph:

Note that, in the years prior to the crisis, the line representing federal government debt roughly parallels the line representing GDP; federal debt wasn’t growing dramatically as a fraction of GDP. So the big post-crisis standoff between Democrats and Republicans over the federal debt wasn’t focused on the big problem.

What was the big problem? Look at the line representing private debt. It clearly is not parallel to the GDP line and, indeed, reflects a rapid growth of private debt relative to GDP.

By itself this isn’t shocking. We all know that a growth in home mortgages preceded the crash, and home mortgages are one kind of private debt—along with other consumer borrowing and borrowing by businesses. What’s more surprising is what we found when we looked at lots of other financial crises around the world, dating back to the 19th century: Though most of these crises aren’t thought of as being fundamentally caused by excessive private debt, the fact is that they were preceded by the same kind of runup in private debt that the U.S. saw prior to 2008.

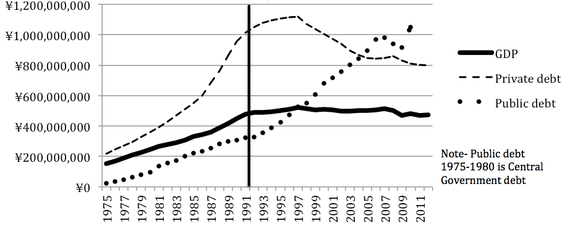

Just to take one example, look at this data from Japan prior to its financial crisis of 1991.

Look familiar? Time and again, that’s the story we found: A major financial crisis is preceded by a runup in private debt relative to GDP. In fact, there seems to be only one other ingredient required for a crisis: that the absolute level of private debt is high to begin with. We found that almost all instances of rapid debt growth coupled with high overall levels of private debt have led to crises.

To put a finer point on it: For major economies, if the ratio of private debt to GDP is at least 150 percent, and if that ratio grows by at least 18 percent over the course of five years, then a big crisis is likely in the offing.

Until the moment of reckoning, things may seem wonderful. Rapid private-debt growth fueled what were viewed as triumphs in their day—the Roaring Twenties, the Japanese “economic miracle” of the ’80s, and the Asian boom of the ’90s—but these were debt-powered binges that brought these economies to the brink of economic ruin.

What’s alarming is that, of the two ingredients for an economic crisis—high private debt and rapid private-debt growth—one is still with us even after the 2008 collapse. Private debt in the U.S., relative to GDP, stands at 156 percent. That’s lower than the 173 percent it reached in 2008, but it’s still nearly triple the level—55 percent—it was at in 1950. Indeed, across the globe there has been a steep climb in the ratio of private debt to GDP over that period.

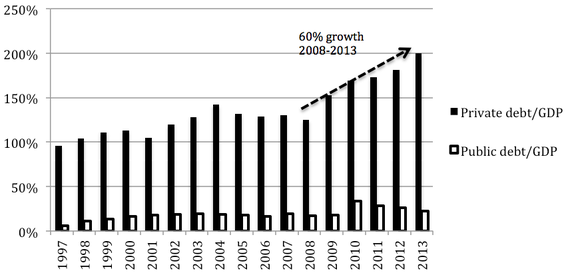

The situation in China is particularly alarming. Look at this graph, which shows changes in the ratio of private debt to GDP and the ratio of public debt to GDP:

Applying our private-debt early-warning criteria to China, we can see that its economy is at risk of a major financial crisis in the near future—a significant concern because of its size and importance to the world economy. China's five-year growth in private credit to GDP is near 60 percent. Its private debt to GDP ratio stands is approaching 200 percent. (As always, data on China's economy must be considered provisional: The numbers for China include “shadow lending” but are somewhat difficult to pin down, and I have seen differing numbers for the current level of private debt in China that range from 167 percent to 200+ percent. But in all cases, the recent five-year private debt to GDP growth trends are above 40 percent.) To be sure, China, by virtue of the government’s large role in the economy, its fiscal assets, and other distinctive features, could forestall the day of reckoning a few years yet. Still the broader picture—extremely high private-debt levels—is alarming.

What’s astonishing is how little attention the global debt problem—the extremely high ratio of private debt to GDP—has gotten. Not only does it leave the U.S. and other countries vulnerable to crisis should brisk growth in that ratio resume, but, quite apart from any crisis, the accumulation of higher levels of private debt over decades impedes economic growth. Money that would otherwise be spent on things such as business investment, cars, homes, and vacations is increasingly diverted to making payments on the growing debt— especially among middle- and lower-income groups that compose most of our population and whose spending is necessary to drive economic growth. Debt, once accumulated, constrains demand.

The ideal condition for growth is to have less capacity (that is, the supply of housing, factories, etc.) than demand, coupled with low private debt. This was the case during the decades immediately after World War II. But now we have nearly the opposite situation. In the first decade of the 2000s, the United States and Europe built far too much capacity, especially in housing, and incurred too much private debt. In the 1980s, Japan built far too much capacity, saddling its banks with too much private debt and too many bad loans. While all these countries have been catching up to this capacity, none yet has less capacity than demand, and all still have high private debt. And now China, whose industrialization and urbanization long fueled global growth, has created its own overcapacity and private debt problem, building far too much capacity in the form of industrial and real estate projects while providing easy credit that fueled a rapid buildup of private debt. So no major global economic player now has that pivotal combination of undercapacity and low private debt that can fuel productive investment and help boost global growth.

What’s more, excessive private debt may contribute to one of the great problems of our time: growing income inequality and the hollowing out of the middle class. The middle class tends to grow when there is too little capacity and low private debt (as after World War II). In contrast, the middle class plateaus or shrinks when there is too much capacity and too much debt (as at the present). Stated differently, inequality increases when there is high capacity and high debt; it decreases when capacity and debt are low.

So what should we do? For starters, rid ourselves of the illusion that if we can rein in government debt we’ll have really tackled the problem. The ratio of government debt to GDP was relatively low, and its rate of growth flat, before the crash of 1929, the Asian crisis of 1997, and the Japan crisis of 1991. In the United States, even with its Middle Eastern wars and a major increase in social program expenditures, the ratio of federal debt to GDP was no higher in 2007 than it had been a decade before. The five-year increases in government debt to GDP in Japan as of 1991 and in South Korea as of 1997 were both near zero. In Spain, before its recent crisis, government debt to GDP declined by 16 percentage points.

To be sure, low government debt has its virtues. Still, the main focus should now be on reducing private debt. This is known as “deleveraging,” and the U.S. did very little of it in the immediate aftermath of the 2008 crisis.

One form of deleveraging is to provide relief for borrowers. This spurs economic growth, because by and large borrowers—especially middle-income and lower-income consumers—are likely to use the extra money to make purchases that stimulate the economy.

So what we need to do is remove some of the debt burden weighing down middle-income and low-income people. You can call it debt “restructuring” or you can call it (partial) debt forgiveness. Either way, it’s needed.

Of course, banks and other lenders may protest. For removing liabilities from the borrower’s balance sheet means removing assets from the lender’s balance sheet. But a one-time program to allow lenders to write down these assets over a long period—say 30 years—will make this sacrifice easily bearable. And as for the much-discussed “moral hazard” problem—the possibility that insulating people from the consequences of their bad decisions will lead to more bad decisions down the road: We briefly suspended our concern regarding moral hazard for lenders when the government rescued them during the crisis. We haven’t done the same for borrowers. And lenders, no less than borrowers, are responsible for the existence of loans that turn out to have been ill-advised.

But none of this is likely to happen until we get over our exclusive political obsession with public debt and gain a proper appreciation of the role private debt plays in economic calamities.